Peptide API Market: Technology Disruption, Innovation Pipelines, and Future Value Creation Across Global Healthcare (2024–2034)

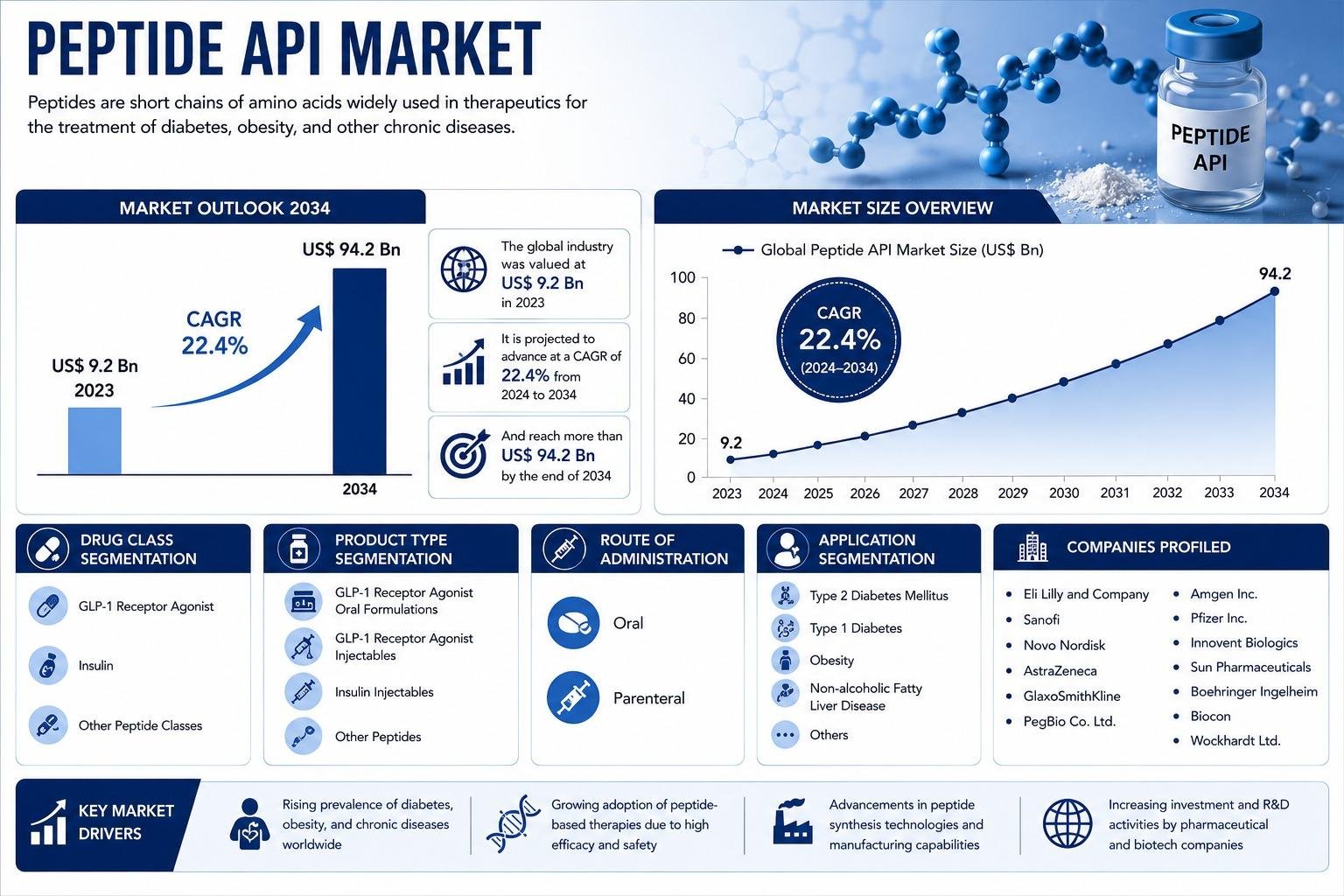

The Peptide Active Pharmaceutical Ingredient (API) market is entering a decisive decade of transformation, driven by the convergence of metabolic disease epidemics, biotechnology advancements, and pharmaceutical innovation centered on GLP-1 receptor agonists and insulin analogs. Valued at approximately US$ 9.2 billion in 2023, the market is projected to exceed US$ 94.2 billion by 2034, expanding at a strong CAGR of 22.4% (2024–2034).

Unlike traditional drug markets, peptide APIs sit at the intersection of chemistry, biology, and advanced manufacturing. Their increasing importance reflects a broader shift in global healthcare toward biologics and targeted therapies that offer higher efficacy, improved safety, and disease-modifying potential rather than just symptom control.

Technological Disruption: The Core of Market Acceleration

1. Evolution of Peptide Synthesis Technologies

One of the most powerful drivers of the peptide API market is rapid advancement in peptide synthesis methods. Modern pharmaceutical manufacturing is increasingly dependent on highly efficient, automated, and scalable technologies.

Solid-Phase Peptide Synthesis (SPPS)

SPPS remains the dominant production technique due to its reliability and precision. Recent innovations include:

- Fully automated synthesizer systems

- High-throughput parallel synthesis capabilities

- Improved coupling reagents and resin technologies

- Enhanced yield consistency across batches

These improvements have significantly reduced production timelines and increased scalability.

Liquid-Phase Peptide Synthesis (LPPS)

LPPS has regained importance for industrial-scale production of longer and structurally complex peptides. It offers:

- Better cost efficiency at large scale

- Improved control over reaction conditions

- Flexibility in producing difficult peptide sequences

LPPS complements SPPS by addressing its limitations in large-scale manufacturing.

Microwave-Assisted Peptide Synthesis

Microwave technology has introduced a major leap in reaction efficiency:

- Faster peptide bond formation

- Reduced reaction times

- Improved purity levels

- Higher yield rates

This method is increasingly used in both research and commercial manufacturing environments.

Recombinant DNA and Biotechnological Production

Recombinant techniques enable peptides to be produced using biological systems such as bacteria, yeast, or mammalian cells. This approach:

- Reduces chemical synthesis dependency

- Enables production of complex peptide structures

- Supports scalable biomanufacturing models

It is particularly important for large therapeutic proteins and peptide analogs.

GLP-1 Innovation Wave: The Strongest Market Disruptor

GLP-1 receptor agonists represent the most transformative force in the peptide API market. These therapies have shifted treatment paradigms in both diabetes and obesity management.

Mechanism of Action and Clinical Impact

GLP-1 drugs mimic a naturally occurring incretin hormone that:

- Stimulates insulin secretion in a glucose-dependent manner

- Suppresses glucagon release

- Slows gastric emptying

- Reduces appetite and energy intake

This multi-mechanistic action makes them uniquely effective in managing metabolic disorders.

Market-Defining Drugs

Key GLP-1-based therapies include:

- Semaglutide

- Liraglutide

- Tirzepatide (dual agonist GLP-1/GIP)

These drugs have become blockbuster therapies, driving unprecedented demand for peptide APIs.

Expansion Beyond Diabetes

Originally developed for type 2 diabetes, GLP-1 therapies are now expanding into:

- Obesity treatment (largest growth driver)

- Cardiovascular risk reduction

- Non-alcoholic fatty liver disease (NAFLD)

- Sleep apnea and other metabolic disorders (emerging research areas)

This expansion significantly broadens the commercial scope of GLP-1 peptide APIs.

Insulin APIs: The Foundation of the Market

Despite the rapid rise of GLP-1 drugs, insulin remains a cornerstone of the peptide API ecosystem.

Market Stability and Demand Drivers

Insulin demand is supported by:

- Persistent global diabetes prevalence

- Lifelong treatment requirement for type 1 diabetes

- Advanced type 2 diabetes progression cases

Innovation in Insulin Therapeutics

Modern insulin development focuses on:

- Ultra-rapid acting formulations

- Ultra-long acting analogs

- Combination therapies with GLP-1 agonists

- Improved biosimilar accessibility

These innovations enhance patient compliance and therapeutic outcomes while maintaining insulin’s central role in diabetes management.

Emerging Peptide Classes and Therapeutic Diversification

The peptide API market is expanding beyond metabolic diseases into multiple therapeutic domains.

1. Oncology Peptides

Peptide-based therapies are increasingly used in:

- Targeted cancer drug delivery

- Tumor receptor targeting

- Immune system modulation

2. Cardiovascular Peptides

Applications include:

- Blood pressure regulation

- Heart failure management

- Vascular function improvement

3. Neurological Peptides

Early-stage research is exploring peptides for:

- Alzheimer’s disease

- Parkinson’s disease

- Neurodegenerative protection mechanisms

4. Endocrine and Rare Disease Applications

Peptides are also used in:

- Growth hormone disorders

- Rare metabolic syndromes

- Hormonal imbalance treatments

This diversification significantly enhances long-term market resilience.

Key Market Drivers

1. Global Rise in Metabolic Disorders

Obesity and diabetes remain the strongest demand drivers. Sedentary lifestyles, poor dietary habits, and genetic predisposition have created a global health burden that peptide therapies are uniquely positioned to address.

2. Aging Population

Older populations are more susceptible to chronic diseases, increasing demand for long-term peptide-based treatments.

3. Pharmaceutical R&D Expansion

Large pharmaceutical companies are investing heavily in:

- GLP-1 pipelines

- Dual and triple agonist development

- Next-generation metabolic drugs

4. Advances in Drug Delivery Systems

Technological improvements are enabling:

- Oral peptide formulations

- Long-acting injectables

- Improved bioavailability solutions

These innovations enhance patient compliance and expand market accessibility.

Manufacturing Evolution and Industry Structure

Peptide API manufacturing is becoming more centralized around advanced facilities and CDMOs.

Key trends include:

- Large-scale aseptic production expansion

- Increased outsourcing of peptide synthesis

- Automation and AI integration in production

- Improved purification and analytical systems

Manufacturing efficiency is now a key competitive differentiator.

Competitive Innovation Landscape

The peptide API market is highly competitive and innovation-driven.

Strategic Focus Areas

Companies are prioritizing:

- Expansion of GLP-1 product portfolios

- Development of next-generation metabolic drugs

- Geographic expansion into emerging markets

- Strategic partnerships and licensing agreements

- Acquisition of biotech startups with peptide pipelines

Major Market Participants

Key companies include:

- Eli Lilly and Company

- Novo Nordisk

- Sanofi

- Amgen Inc.

- AstraZeneca

- Pfizer Inc.

- Boehringer Ingelheim

- Biocon

- Sun Pharmaceutical Industries

- Wockhardt Ltd.

- Innovent Biologics

- PegBio Co. Ltd.

These firms are leading innovation in metabolic disease therapeutics and peptide manufacturing technologies.

Future Outlook (2024–2034)

The peptide API market is expected to undergo structural transformation:

- GLP-1 therapies will remain dominant growth engines

- Oral peptide formulations will gradually reduce injection dependency

- Dual and multi-agonist therapies will redefine treatment efficacy

- AI-driven peptide discovery will accelerate innovation cycles

- Manufacturing automation will reduce production costs

- Therapeutic applications will expand beyond metabolic diseases

Overall, the market is transitioning from a niche biologics segment to a core pillar of global pharmaceutical innovation.

Conclusion

The peptide API market is being reshaped by disruptive technologies, expanding GLP-1 applications, and rapid pharmaceutical innovation. As manufacturing capabilities evolve and therapeutic applications broaden, peptide APIs are set to become a foundational component of next-generation global healthcare systems.

Категории

Больше

Compétences et stratégies d'Ifa Ifa, souvent appelé Saurovéto, est bien plus qu’un simple vétérinaire. En plus de ses compétences médicales, il est aussi un combattant redoutable. Ce guide vous expliquera comment exploiter au mieux ses talents en jeu. Dernière mise à jour : version 5.8. Reconnue à travers...

2018 MMO Outlook As 2017 wraps up and the momentum for 2018 continues to build, the Massive Overthinking crew has gathered once more to share their daring and playful forecasts for the upcoming year. Reflecting on our previous predictions, which proved to be quite accurate, we’re feeling confident about what’s on the horizon for the MMO landscape. So, what trends and surprises...

Recent surveys reveal a concerning trend among home computer users regarding malware protection. In a study of Mac and Windows PC owners, it appears that only a small fraction of Mac users have actively installed anti-malware solutions on their primary devices. Conversely, a significant majority of Windows users—around 86%—report having such security measures in place. These...

Depuis sa sortie, Genshin Impact a rapidement captivé un large public grâce à son esthétique rappelant celle de The Legend of Zelda : Breath of the Wild. Les chiffres de ses revenus ne cessent de croître, attestant de son immense popularité. Selon Sensor Tower, le jeu aurait généré environ 60 millions de dollars seulement durant la...

Marché Nocturne Valorant Tous les quelques mois, Riot Games étonne la communauté de Valorant avec un événement spécial appelé le Marché Nocturne. Il s’agit d’une boutique temporaire en jeu où les joueurs peuvent acheter des objets à prix réduits. Contrairement aux mises à jour classiques du magasin,...