The Multifaceted Benefits: Deconstructing the Credit Card Market Value Proposition

The immense and enduring Credit Card Market Value is derived from the multifaceted benefits it provides to every participant in the payment ecosystem: consumers, merchants, and the financial institutions that power the system. For the end-user, the credit card has evolved from a simple payment device into a powerful financial tool that offers a unique combination of convenience, security, and purchasing power. The market's value is not just in its ability to facilitate transactions but in the entire ecosystem of services and benefits that have been built around it. It represents a sophisticated solution that addresses fundamental needs for short-term liquidity, fraud protection, and a more rewarding and seamless commerce experience. Understanding this value proposition from the perspective of each stakeholder is key to appreciating why the credit card has remained such a dominant and resilient force in the global economy, even in the face of constant technological disruption and the emergence of new payment methods. It is this well-rounded value delivery that underpins the market's multi-trillion-dollar scale.

For consumers, the value proposition is clear and compelling. The most immediate benefit is convenience. Credit cards eliminate the need to carry large amounts of cash and provide a universally accepted method of payment for both in-person and online purchases. Beyond convenience, they provide a crucial layer of security. If a card is lost or stolen, or if a fraudulent transaction occurs, consumer liability is typically limited or zero, a level of protection that cash or debit cards often cannot match. This fraud protection provides peace of mind and encourages participation in e-commerce. The "credit" aspect itself is a core part of the value, offering a revolving line of credit that can be used for large purchases or to manage cash flow between paychecks. Finally, the rewards ecosystem provides tangible monetary value. By using their cards for everyday spending, consumers can earn cash back, airline miles, hotel points, or other valuable perks, effectively receiving a discount on their purchases. This combination of convenience, security, credit access, and rewards creates a powerful and sticky value proposition for the cardholder.

From the merchant's perspective, the value of accepting credit cards, despite the associated costs, is undeniable. The primary benefit is a significant increase in sales. Studies have consistently shown that consumers tend to spend more when using a credit card compared to cash. Accepting cards also expands a merchant's potential customer base, particularly in the e-commerce space where it is the primary payment method. It streamlines the checkout process, reducing wait times and improving customer satisfaction. Furthermore, credit card payments improve a merchant's cash flow and reduce the risks and logistical challenges associated with handling and depositing large amounts of physical cash. While the interchange fees charged on each transaction are a significant consideration, most merchants view them as a necessary cost of doing business, an investment that is more than offset by the higher sales volumes, operational efficiencies, and improved customer experience that card acceptance enables. For a modern business, not accepting credit cards is to willingly place a major barrier between themselves and the majority of their potential customers.

For the financial institutions—the issuing banks and the payment networks—the value is, of course, financial, but it is also strategic. For issuers, credit cards are one of the most profitable products in consumer banking, driven by interest income and fee revenue. More than that, a credit card relationship is a gateway to a deeper, more holistic banking relationship with a customer. A satisfied cardholder is more likely to use the same bank for their checking account, mortgage, and investment services, increasing their lifetime value to the institution. For the payment networks like Visa and Mastercard, the value lies in their role as the central toll collectors of global commerce. By operating the vast, secure, and interoperable networks that connect millions of banks and merchants, they earn a small fee on trillions of dollars in transactions, creating a highly scalable and profitable business model. The data generated by these transactions is also an incredibly valuable asset, providing deep insights into consumer spending trends that can be monetized through analytics and consulting services.

Top Trending Reports:

Категории

Больше

The extraction-shooter scene has grown from a narrow specialty into a bustling genre with multiple contenders. Where Escape from Tarkov once stood almost alone, newer projects like Arc Raiders and Marathon are joining the field. Virgil Watkins, design director at Embark Studios, told GamesRadar+ that breaking into multiplayer live services is difficult because expectations are so high and many...

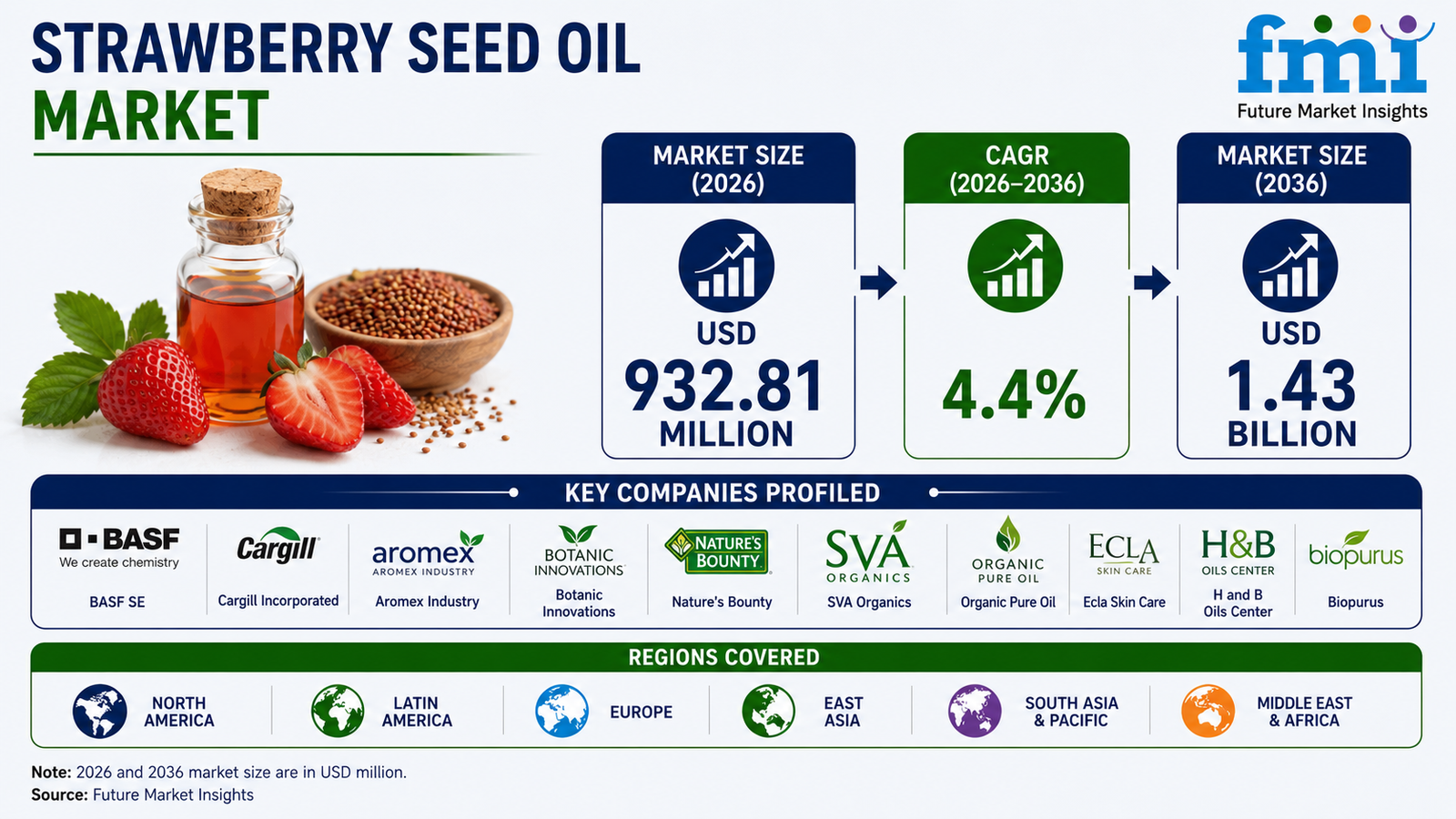

NEWARK, Del., USA | May 18, 2026 — According to Future Market Insights (FMI), the global strawberry seed oil market is experiencing steady growth, supported by rising consumer demand for natural and botanical skincare ingredients, expansion of clean beauty product categories, and increasing adoption of antioxidant-rich plant-based oils across personal care and wellness...

A high-octane collaboration is set to electrify screens worldwide. Netflix and Skydance Media are joining forces for a major new action film, "Six Underground." This project marks a significant first, being the inaugural event-level feature film partnership between the two companies. At the helm is acclaimed director Michael Bay, known for his blockbuster spectacles. Starring in the lead role...

A recent leak about Honkai: Star Rail has shed light on several anticipated updates set for version 3.2, reflecting Hoyoverse's consistent update rhythm of approximately every six to seven weeks. Since the game's launch in April 2023, its second anniversary is approaching, and it is widely expected to be celebrated within this upcoming patch. Although official details remain under wraps, leaks...

Delta Force, developed with Unreal Engine 5 and currently in early access beta, delivers exceptional performance on PC systems. Utilizing advanced upscaling techniques, the game can surpass the refresh rate limitations of high-quality monitors, even when configured at higher graphics settings and resolutions. However, optimizing your graphics settings can significantly enhance gameplay...